When KPIs Look Good but Processes Fail

Why this mismatch happens and how to close the gap

Most organizations that have invested in process improvement recognize these four names: Procure-to-Pay, Order-to-Cash, Record-to-Report, and Hire-to-Retire. They appear in ERP implementations, shared services design, and process maturity assessments across industries and geographies.

What remains less understood is why all four resist meaningful improvement, not marginal optimisation but structural change, consistently across organisations and sectors.

This article maps these four process families, examines what makes each structurally distinct, and highlights the governance pattern they share. It is the second in a series on why BPM investments tend to plateau at mid-level maturity.

Two Problems You Have Seen Before

Consider a familiar sales problem. A customer complains about a late delivery and a missing invoice. Sales confirms the order was placed correctly. Production confirms it was manufactured on time. Logistics confirms the shipment went as planned. Finance confirms the invoice was issued according to procedure.

In most organizations, no one owns the problem as a whole. Each function has performed correctly within its own perimeter. No one has visibility of the full timeline, from order confirmation to payment, that would reveal where the cycle actually broke down.

The incentive misalignment surfaces next. The customer delays payment. Finance applies a late fee according to policy. Sales pushes back. This is a strategic account, and the fee risks the relationship. Finance responds that days sales outstanding is already above target and that payment terms must be enforced. The issue escalates.

What remains unspoken is this. Sales already hit its target. The invoice was issued, revenue was booked, and the bonus secured. Whether cash actually arrives, and when, is someone else’s problem.

This is not cynicism. It is rational behavior. Sales measures what it controls. The invoice was sent, the order was correct, the revenue recognized. Payment depends on credit terms and collection activities owned elsewhere. The issue is not the metric. The issue is that no one owns the end-to-end metric.

This is not a sales problem. Nor is it a finance problem. It is an Order-to-Cash problem. No one owns Order-to-Cash.

The KPI structure makes the conflict inevitable. Sales is measured on invoiced revenue. The target is achieved the moment the invoice goes out. Logistics is measured on OTIF, on time and in full, which ends when goods leave the warehouse. Finance is measured on DSO, which only begins once the invoice is issued. Three functions. Three clocks. None aligned.

In most cases, no one is measured on whether cash actually arrives or how long the full cycle takes.

A process-oriented KPI would make the failure visible. Order-to-cash cycle time, or the share of orders fulfilled, invoiced, and collected without exception. No single function can own such a metric. A process owner can. In most organizations, there is none.

Now consider a familiar procurement problem. Purchasing negotiates framework agreements to lower prices, yet total procurement cost does not fall. Purchasing blames Finance. Too many invoices fall outside agreements. Finance blames Production. Orders are placed without requisitions. Production blames Purchasing. The agreements do not cover what is actually needed.

Maverick spend persists because no one measures Procure-to-Pay as an integrated flow. Requisitions are bypassed because no one owns the process required to enforce them. When the issue surfaces in a budget review, it appears to be a discipline problem. It is not.

Again, the KPI structure drives the outcome, and in some cases rewards the wrong behavior. Purchasing is measured on price variance, which registers nothing when contracts are bypassed. Production is measured on supplier delivery reliability, creating pressure to order through the fastest available channel. Agreements become optional. Finance is measured on cost per invoice processed. This is a legitimate efficiency metric that is, paradoxically, improved by maverick spend. Fewer purchase orders create simpler processing flows.

Finance is not optimizing incorrectly. The metric is well designed for what Finance controls. The problem lies in what all three functions optimize simultaneously. Each KPI is locally rational. Together, they produce a system that rewards bypassing the process.

A process-level KPI would expose the gap immediately. Maverick spend rate, or the percentage of orders initiated with a purchase requisition. That metric belongs to a process owner. In most organizations, there is none.

These are not edge cases. They are the default state in organizations with strong functional structures but weak process ownership, where no one has the authority, visibility, or accountability for end-to-end outcomes.

Understanding why requires a precise definition of what a process family actually is.

What a Process Family Is and Isn’t

A process family is not a department or a function. It is an end-to-end flow of work that crosses multiple functional boundaries, beginning with a trigger and ending with an outcome.

Large organizations are typically structured around a small number of core functions such as Sales, Production or Service Delivery, Logistics, Procurement, Finance, and HR. Each is optimized for within-function performance, with its own KPIs and reporting lines.

Process families cut across all of these. In day-to-day operations, a process does not operate as an integrated whole. It runs as a sequence of handoffs between units that optimize locally.

This is exactly why the problems described earlier persist. It also explains why each process family behaves in distinct ways once you look at its structure rather than its functions.

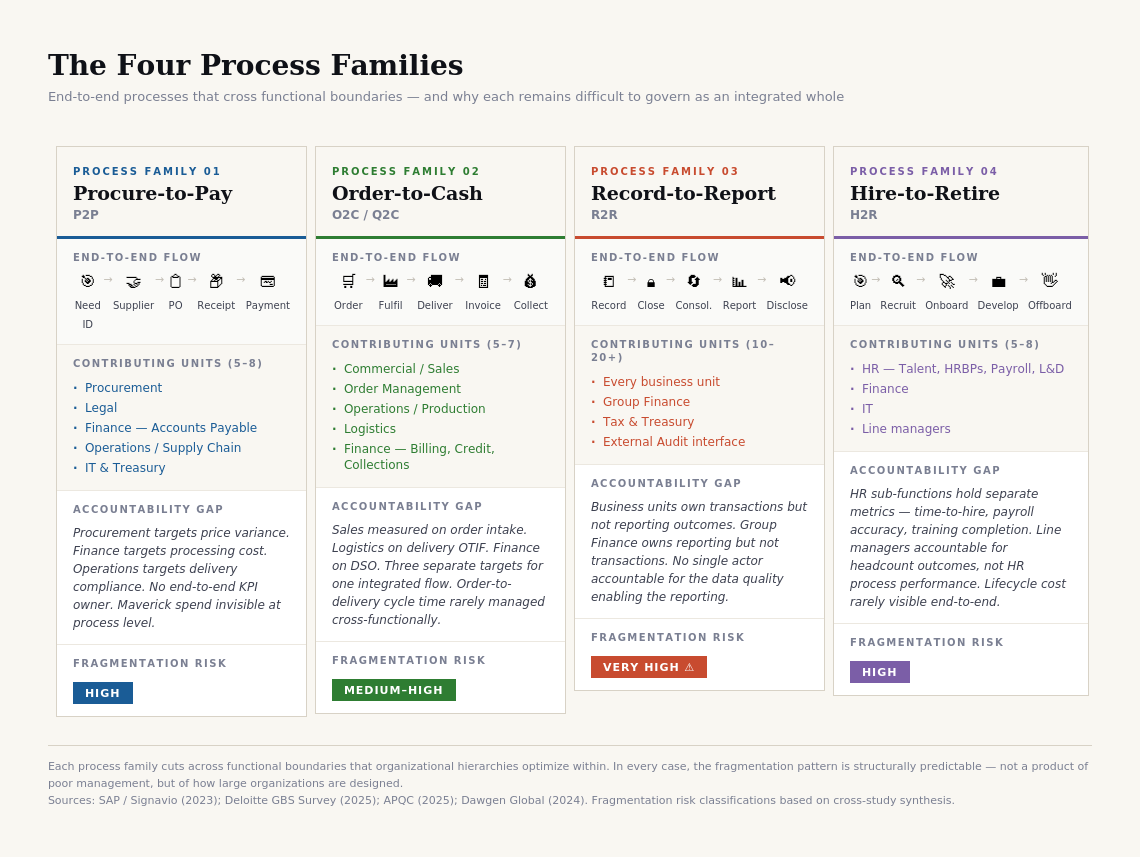

Figure 1: The Four Process Families

The Four Families

Each process family shares a structural property: it spans the functional configurations large organizations actually use in a way that makes integrated accountability predictably fragile.

Procure-to-Pay covers the full cycle from need identification through supplier selection, purchase order creation, goods receipt, and payment. It typically involves five to eight contributing units. The accountability gap is predictable. Procurement targets price variance. Finance targets processing cost. Operations targets delivery compliance. These are separate metrics applied to a single integrated process, and no one is accountable for the whole. The underlying issue is the same as in the O2C case. No one has a process-level view.

Order-to-Cash connects a customer order to cash receipt, passing through order management, fulfillment, logistics, billing, and collections. Sales is measured on order intake. Logistics on delivery performance. Finance on days sales outstanding. Separate targets. Separate reporting lines. One process. Order-to-delivery cycle time, the metric that would reveal end-to-end performance, is often not tracked or managed across functions.

Record-to-Report is the most structurally complex of the four. It integrates transactional accounting from every business unit with group-level consolidation, reporting, and external disclosure. The number of contributing units can reach twenty or more. The accountability gap here is inverted. Business units own the transactions but have no stake in reporting outcomes. Group finance owns the reporting but does not control the transactions. In many large organizations, no single actor is accountable for the data quality that determines whether financial statements can be trusted. Close cycle time, the clearest end-to-end metric, is rarely managed as an integrated process outcome.

Hire-to-Retire spans the full employee lifecycle, from workforce planning and talent acquisition through payroll, development, and offboarding. HR sub-functions hold separate metrics such as time-to-hire, payroll accuracy, and training completion rates. Line managers are accountable for headcount outcomes but not for the HR process performance that underpins them. End-to-end workforce lifecycle cost is often not visible to any single actor.

These four families appear in virtually every large organization, regardless of industry. Other process families follow the same structural logic. The names change. The pattern does not.

Issue-to-Resolution spans customer service, technical support, and back-office operations. Customer service is typically measured on first-contact resolution. Technical support on ticket closure time. Back-office on SLA compliance. Separate clocks for one customer experience.

Bid-to-Bill, common in project-based organizations, runs from commercial proposal to final invoice. Sales owns the margin at bid. Delivery owns the cost at execution. Finance owns the invoicing. No one owns the gap between bid margin and realized margin.

The Pattern They Share

What stands out is not the differences between these process families, but how similar they are. In each case, the contributing units are known. The accountability gaps are known. The missing metrics are known. Yet the gaps persist, year after year, across organizations that have invested seriously in process improvement.

These organizations are not unaware of the problem. They are unable to resolve it with the tools they currently use. APQC has tracked “defining and mapping end-to-end processes” as the top process management priority for several consecutive years, cited by around 40 percent of organizations in its 2025 survey (APQC, 2025). The priority remains. The outcome does not change.

This points to something structural. These process families are not difficult to improve because of insufficient effort, weak methodology, or lack of executive attention. They are difficult because each cuts across the coordination logic of the organization.

Each function is optimized for its own performance. The process depends on shared accountability across functions. The tension between the two is built into the design.

What Advancing Beyond Level 3 Would Change

Both cases share the same underlying condition. Functional KPIs are present and working. Process-level accountability is absent. This defines Level 3 and is exactly what Level 4 requires an organization to resolve.

At Level 3, the O2C scenario unfolds as described. The issue escalates into a management discussion that should never have been necessary. The process owner appears on the organization chart but lacks a consolidated view of order-to-cash cycle time, has no authority to realign incentives across Sales and Finance, and carries no direct accountability for whether cash arrives on time. The role exists. The governance does not.

At Level 4, the same situation plays out differently. The process owner has access to integrated performance data: order-to-cash cycle time, first-time-right rate, and percentage collected within terms, across all contributing functions, updated at least monthly. When DSO deteriorates, the root cause is visible. It can be traced to credit decisions, billing errors, or breakdowns between logistics and invoicing. The process owner can convene the relevant functions and require action without escalating to the CFO. Because the role is evaluated on end-to-end outcomes, the incentive to act is built into the structure.

For Sales, one practical change stands out. Late payment disputes no longer land with the sales team. When a strategic customer delays payment, the process owner is responsible for investigation and resolution. Sales retains its invoicing metric. What changes is that someone else now owns the end-to-end result, with the authority and visibility to act. The conflict remains, but it is handled at the right level.

In Procure-to-Pay at Level 3, maverick spend remains largely invisible because the process is not measured as a whole. Purchase requisitions are bypassed because the process owner lacks authority over ordering behavior in Production. At Level 4, maverick spend becomes a visible metric with clear ownership. The process owner has both the data to detect it and the mandate to address it, including the ability to work with Finance to adjust the cost-per-invoice KPI that currently encourages bypassing the process.

In Record-to-Report, the most structurally complex case, Level 3 means close cycle time is not managed end-to-end. It reflects whatever each business unit delivers, while group finance lacks the authority to enforce consistent data quality. At Level 4, the process owner tracks a first-time-right rate at entity level, the share of submissions requiring no restatement. This exposes data quality issues early and creates a basis for structured engagement with business unit CFOs, rather than relying on periodic escalation.

Moving from Level 3 to Level 4 does not require a new methodology or a new governance model. It requires making the existing process owner role operational. That means end-to-end visibility, cross-functional authority, and incentives tied to process outcomes.

Without all three, the KPI conflicts described earlier are not management failures waiting to be resolved. They are structural features of the organization, as predictable as the processes themselves.

What This Means Before Your Next Process Investment

Before investing further in any of these process families, whether in a new governance structure, a new system, or a redesigned operating model, a more basic question needs to be answered. Do the structural conditions for cross-functional accountability actually exist?

If you have read the first article in this series, these three questions will be familiar. They are repeated here deliberately. They apply to every process family described above, and the answer is often different in each case.

An organization may have the conditions in place for Procure-to-Pay, but not for Record-to-Report. The diagnosis is not organizational. It is process-specific.

Three questions determine this:

Does the process owner have integrated performance data spanning all contributing units, not just functional reports, but a consolidated end-to-end view?

Does the process owner have the authority to approve improvements that require changes across multiple functions, without separate sign-off from each function head?

Does the process owner’s performance evaluation include at least one end-to-end process KPI with meaningful weight?

If the answer to any of these is no for a given process family, the structural conditions for effective governance are not in place. Additional investment will create more infrastructure. It will not create more maturity.

#BPM #ProcessManagement #OperationalExcellence #ProcessImprovement #BusinessTransformation #P2P #O2C #R2R #H2R #KaldLabs

A strong perspective on why functional optimization alone cannot deliver better cash outcomes. Order-to-Cash performance depends on alignment across sales, operations, billing, and collections, with clear ownership of the full process rather than individual metrics. Governance is often the missing link in working capital improvement.